Balance sheet: explanatory note to the balance sheet. Form, sample

The organization's financial statements must give a reliable picture of the organization's financial position as of the reporting date, the financial result of its activities and cash flows for the reporting period (Part 1, Article 13 of the Federal Law of December 6, 2011 No. 402-FZ). Users make economic decisions based on financial statements. That is why the composition of the statements is not limited to just the balance sheet and financial statements. Explanations are usually prepared for two main forms. Explanations for the balance sheet and financial results statement include appendices to these forms and an explanatory note (clause 5 of PBU 4/99). The appendices to the balance sheet and the income statement are a statement of changes in capital, a statement of cash flows and a report on the intended use of funds (clause 2 of Order of the Ministry of Finance dated July 2, 2010 No. 66n). What is an explanatory note?

Explanatory note to the balance sheet and income statement

An explanatory note to the balance sheet and other forms of reporting is not a mandatory document and is drawn up at the discretion of the organization. Therefore, the composition and structure of the explanatory note is different for each organization. The purpose of the explanatory note is to provide users with additional data that is not included in the main reporting forms and annexes to them, but which would be useful for reporting users. For example, the explanatory note reflects significant events that occurred after the reporting date. An example of such information would be information about annual dividends recommended or declared after December 31 based on the organization's performance for the reporting year (

In accounting practice, the degree of disclosure is established as necessary and depending on the supervisor. Thus, to submit a balance, some indicators can be specified upon command (to the head office), and others for the tax office.

What is an explanatory note to financial statements

The definition of accompanying documentation is based on the provisions of Article 5 of the Accounting Regulations (RA) 4 of 1999.

The document itself usually contains a breakdown of key indicators of the enterprise that are of interest to inspection authorities or. The note may include estimates such as turnover ratio, profitability, or inventory ratio. Numerical parameters are calculated based on the lines of the balance sheet.

A significant part of the content is a description of the reasons for the formation of receivable and creditor types, the consequences of an increase or decrease. If in the reporting period there was a bonus (de-bonus) for the positions of workers, employees, and managers. Often the note indicates the facts of the movement or disposal of large assets, the reasons (orders for the enterprise).

The video below will tell you what an explanatory note to financial statements is:

Concept and regulatory framework

The main regulatory act for the purpose of drawing up a note with explanations is PBU 4 of 1999. This regulatory document establishes the need to form a document, but does not reflect its content. The structure and degree of information disclosure is determined by enterprises based on requests from affiliates and regulatory authorities. Again, if the founders have the right to receive comprehensive information about the actual state of affairs at the enterprise, then for tax and statistics information disclosure occurs to a degree sufficient for monitoring.

When drawing up a template for an explanatory note, you can refer to the Accounting Law. The standard provides approximate names of sections in which essential information about the enterprise should be clarified.

Composition and role

- According to the same PBU 4 of 1999, the composition of the explanatory note is determined by requests and internal (local) regulations. The procedure for disclosing information is fixed in;

- For the purpose of preparing for writing an audit report, the organization turns to the requirements (requests) of the auditors to draw up. In the absence of an explanatory note as part of the applications, there is a risk of receiving a remark about the incomplete submission of forms or receiving a request for the submission of an additional set of reports.

In the absence of an explanatory note, you can not only encounter an incorrect interpretation of reporting indicators, but also, as provided for in the Tax Code, Article 126. The chief accountant will also be given a sense of the level of responsibility in accordance with the Administrative Code, Article 15.6.

Procedure for leaving

Due to the fact that there is no uniform template for filling out in governing documents and albums, enterprises usually use their own accompanying document forms. As a rule, a note contains several sections, each of which reveals certain production indicators and determines the results of activities for the reporting period. The explanatory paragraphs are again developed taking into account the practice of accessing this reporting form.

The standard structure of an explanatory note is as follows:

- General information. Here the legal information of the control object, the status of the company, and types of activities are disclosed. If this does not contradict the Corporate Code, the number of employees on staff may be indicated;

- Excerpt from the accounting policy regarding the display and collection of indicators for reporting;

- Analysis of the numerical parameters of the balance sheet, analysis of the dynamics of the main indicators of the profit and loss statement. A minimum of five major suppliers and five consumers are indicated here;

- The organization's plans for the future, for example;

- Significant events since the last report was submitted;

- Loans received, financial assistance, participation in government programs;

- Conclusion.

Forms

Since there is no single form for drawing up a note, it is preferable to fix its form in an appendix to the accounting policy. This eliminates the possibility of unjustified changes to sections of the report when changing officials or going on vacation. The manager must also understand that it will not be possible to easily add or remove some sections; he will have to confirm his decision in writing.

The PZ form can be downloaded for free.

Explanatory note of financial statements (filling sample)

The principles of preparing financial statements along with the PP are described in this video:

Reporting period

Most often this is a year. For verification purposes, a snapshot of indicators can be requested for a shorter period. In any case, accountants should not despair, since information in the early period will later become the basis for drawing up the final note.

By whom and where is it provided?

An explanatory note as an integral appendix to the balance sheet, budget of income and expenses or cash flow statement, is prepared by the accounting department or a responsible employee of the financial department. It all depends on the status of the requested enterprise.

For example, the accounting department can prepare an application for the tax office, and for submission to a higher authority. In any case, the actions of specialists must be coordinated. Differences in information may be formal, but must be taken from official records.

Submission procedure

Together with reporting forms in paper form or a scanned copy via communication means.

Audit of PZkBO

Analysis of the note reveals the following:

Analysis of the note reveals the following:

- Completeness of information;

- Are key indicators deciphered (profit, taxes, deviations from the norm);

- Is it shown, including disposal;

- Doesn't the enterprise hide the possible;

- Degree of competence in conducting internal analysis;

- Is the company developing in the future?

To carry out the analysis, the controlling body can use financial formulas to calculate the parameters of interest or indicate the need for such calculations in the content of the explanatory note.

An explanatory note can be created in 1C: Consolidation 8, as the video below will tell you about:

Any enterprise reporting will be clearer for information users if there are explanations. Financial and accounting statements include an explanatory note to the balance sheet and financial results statement. Let's look at a sample of filling out the notes to the balance sheet.

Explanations drawn up for financial and accounting statements are intended to:

- reveal in detail the meaning of reporting indicators;

- link the contents of reports to each other;

- reflect the current accounting policy of the enterprise;

- justify the obtained financial result.

This is an important document, based on which you can conduct an in-depth analysis of the organization’s economic activities.

All organizations that maintain full accounting records must draw up an explanatory note. The exception is small enterprises that are allowed a simplified accounting procedure and are not subject to mandatory audit.

The law does not establish a mandatory form of presentation; it can be formatted using tables and text. There is only the form recommended by the Ministry of Finance.

Deadlines and procedure for submitting an explanatory note

The explanatory note is drawn up within the same time frame as the accompanying financial statements. The presentation procedure also coincides with the procedure, deadline and recipients for submitting annual or interim accounting and financial statements.

Get 267 video lessons on 1C for free:

Contents of the explanatory note to the balance sheet

In the process of drawing up explanations, it is necessary to disclose the indicators shown in the reports in aggregate:

- cost of fixed assets;

- value of intangible assets;

- inventory cost;

- accounts payable;

- accounts receivable;

- structure and size of financial investments.

It should also be taken into account that the content of not only balance sheet items is disclosed, but also other forms of reporting, especially with regard to the Statement of Financial Results.

Almost always, if an enterprise receives a loss at the end of the reporting period, the tax authority requires it to be justified and to confirm the correctness of accounting for income and expenses. In this situation, a combination of balance sheet indicators, cash flow statement, and statement of changes in capital can confirm the correctness of tax calculations.

If the company changed its accounting policy, then it is necessary to reflect this in the text and explain the essential conditions of the accounting policy.

The explanatory note also discloses the composition of affiliated entities.

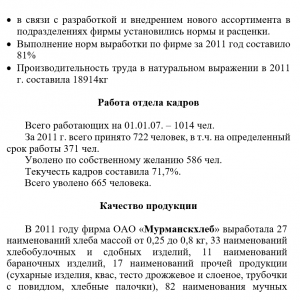

Sample explanatory note to the balance sheet

Example 1. How to start an explanatory note

Example 2. How to explain individual balance sheet items

In the explanatory note we provide, for example, the following tables, explaining which indicator is indicated in the corresponding line of the balance sheet.

Example 3: How to Explain an Income Statement

With careful and systematic maintenance of tax accounting registers, it will not be difficult for an accountant to enter accounting results into a simple table. In this case, the cost structure of the enterprise is clearly visible.

This method of explanation is also convenient for further preparation of the Report for the founders. The visibility of expense items allows the owner to make adequate decisions and assess the profitability of business areas.

If an enterprise receives income from several types of activities, it is also advisable to break down the gross income received into individual items:

Thus, a competently and fully drawn up explanatory note addresses the following issues:

- reduces the number of requests for explanations received by the organization from tax authorities;

- reduces the likelihood of on-site inspections;

- gives reporting users the most accurate picture of the organization’s economic life;

- serves as the basis for deep analytics of business processes;

- helps owners correctly assess the situation and develop profitable areas.

Drawing up an explanatory note is no less a painful task for an accountant than preparing the balance sheet itself.

An explanatory note is an independent form of accounting reporting, its most important, voluminous part.

Often, the text of an explanatory note can be located on 100 or more typewritten sheets. Regulated by clause 5 of PBU 4/99

What is an explanatory note?

This is a document that includes a written explanation of the figures contained in the balance sheet, as well as the profit and loss statement and their applications.

The basic principles when writing an organizational explanatory note include the principles of materiality and comparability.

If we talk about comparability, we mean a comparison of the quantitative values of a number of items in the accounting report over a period of time (a number of years).

We compare only essential items so as not to violate the principle of rationality when preparing reports

They have the opportunity not to attach an explanatory note to the balance sheet when submitting reports provided by the state to small enterprises.

The explanatory note to the balance sheet should consist of the following sections with disclosure of information for each of them:

1. Information about the organization

This section is informational and descriptive in nature.

The name, as well as the established organizational and legal form of the company, is indicated.

In addition, this section indicates the legal and actual addresses, information about the founders of the organization, and the size of the authorized capital.

The organizational structure of the organization is also indicated, as well as the availability of licenses and permits available to the organization and their validity period.

Financial information indicates the amount of taxes that the organization paid in a given year and the average annual number of employees employed in the organization.

Information about the company’s auditor (name, legal address, etc.) is also indicated.

2. Enterprise accounting policy

The content of the organization's accounting policy, its main changes over the past year compared to the previous year, as well as the reason for the changes in the accounting policy are described.

The organization also specifies separate rules for accounting for assets and liabilities.

3. Information about the main assets and liabilities of the organization

In this subsection, information is disclosed under the following headings:

- by fixed assets (depreciation, movement of fixed assets,

- information about real estate objects that are under state registration, etc.),

- on credits and loans (availability of credits and loans, their repayment terms, as well as complete information on them, including information on weighted average values for loans and borrowings),

- on inventories (methods of their assessment and consequences),

- on financial investments (all information regarding securities is disclosed),

- for assets and liabilities (the amount of exchange rate differences that are attributed to financial results, and also the value of the official exchange rate of the Bank of Russia as of the reporting date is indicated).

4. Assessing the structure of the organization’s balance sheet

The main purpose of compiling this section is to assess the enterprise and its financial condition within both the short-term and long-term periods.

To assess the financial condition of an enterprise in the short term, indicators such as:

- liquidity ratio,

- financial dependence,

- profitability,

- solvency.

For the long term, an indicator such as the organization’s dependence on external creditors and loans is calculated

5. Information about the organization’s income and expenses

Information is indicated under the relevant items of the enterprise's balance sheet.

6. Explanations required for the main reporting items

Information is indicated if the items are material and at the same time this disclosure is absent in the financial reporting forms.

7. The business activity of the organization is assessed

The market in which the company operates is assessed, as well as the organization’s business reputation, which is formed, among other things, by the fame of its clients.

Planned indicators and the degree of their implementation are also assessed.

8. Explanation of opening balances and their changes

The size of the change in opening balances and the reasons for this change are indicated (reorganization of the enterprise, introduction of new accounting requirements, etc.).

9.Information about affiliates

Information related to affiliated persons is disclosed in detail, namely:

- a complete list of such persons,

- the nature of the relationship with them,

- types of transactions with affiliates

10. Conditional facts on organizational economic activities

Contingent liabilities include

- warranty obligations of the organization,

- her participation in court proceedings,

- the amount of guarantees issued by the organization.

This paragraph discloses complete information on contingent facts, if any.

11. Joint activities of the organization

The purposes for which the enterprise conducts joint activities are indicated, as well as the amount of assets invested in this activity, complete information on jointly carried out operations.

12. Data on organization segments

The section is filled out only by organizations that have subsidiaries and dependent companies, as well as if associations and unions are entrusted with the preparation of consolidated general financial statements in accordance with the constituent documents.

13. Declaration of events that occurred after the reporting date

The cause and nature of the event that occurred, as well as the possible consequences of the event that occurred, are described.

14. Government funding

If the organization received government assistance, then its amount, financing purposes, other forms of government support, as well as outstanding provision of budget funds as of the reporting date are disclosed.

15. Environmental factors

Reflected if there is a fact of negative impact on the environment.

This paragraph contains an indication of the degree of impact on the environment, as well as measures taken by the organization to protect the environment.

16. Information in accordance with PBU 18\02

Contains a complete reflection of accounting calculations for corporate income tax.

17. Information disclosed by joint stock companies

The number of shares issued during the reporting period is indicated.

Indicates shares that have been issued and fully paid, and may also be unpaid or partially paid.

Information on additional issue of shares of the company is disclosed

18. Data on discontinued operations

Full information is provided on the reasons for the termination of a particular type of activity, the value of assets and liabilities disposed of or repaid as part of the termination of the activity and other information on this activity are indicated.

19. Other information

Information is indicated that was not previously disclosed in the explanatory note.

For example, it reflects the efficiency of the organization, the competitiveness of products, sales markets, etc.

Each company builds its own structure and composes it only from those sections that directly relate to the nature of the organization’s activities.

Explanatory note to the balance sheet sample

The rules by which the organization's financial statements are prepared were approved by Order of the Ministry of Finance No. 43n dated July 6, 1999. PBU 4/99 defines the structure of the documentation. An explanatory note to the balance sheet serves as its integral elements. Let's look at this document in detail.

General information

As mentioned above, the financial statements of an organization include several elements. These include:

- Audit report. It confirms the accuracy of the balance. The conclusion is provided by those enterprises for which, according to the standards, a mandatory audit is provided.

- Final document on financial results.

- Balance sheet.

- Explanations.

- Applications.

Explanatory note to the balance sheet

This document discloses the information present in the final accounting documents. The explanatory note to the balance sheet must contain information about:

Important point

The explanatory note to the balance sheet should also include a description of the facts of non-application of PBU in cases where their use does not allow a reliable description of the property status and financial results of the company, with justifications. Otherwise, the relevant circumstances will be considered as non-compliance with the rules and act as a violation of legal requirements. Accordingly, control authorities can apply sanctions provided by law against those responsible.

Additional Information

In addition to basic data, an accounting note may include information that accompanies the final documents if the management of the enterprise decides that they will be useful to users when making management decisions. Additional information includes:

The explanatory note to the balance sheet may contain other additional information. If necessary, this data can be presented in the form of charts, graphs or analytical tables.

Example of an explanatory note

The document is drawn up according to approved rules. An example explanatory note consists of the following sections:

- Basic information about the enterprise.

- Revenues from sales.

- Expenses associated with the sale.

- Financial result obtained from the main activity.

- Other income.

- Other expenses.

- Calculation of income tax.

- Financial result of economic activity.

- Information about accounting policies.

Basic information about the company

The explanatory note to the balance sheet begins with it. The form of the document is not unified. The company has the right to independently develop the form. The section on basic information about the enterprise should contain:

The basic information also indicates the number of employees, information on the size of the authorized capital, and main types of activities.

Income/expenses from sales

The explanatory note to the balance sheet discloses data on income and expenses received/made during the performance of work, provision of services, as well as the sale of goods. The document indicates specific figures for certain periods (by year). The resulting difference in accounting for management and production costs must be justified. In this case, specific calculations are provided.

Financial result from core activities

The accounting note contains indicators for the current reporting period. In this case, the amount of profit for tax purposes is indicated. If any information is not reflected in the balance sheet, this fact is explained in the note. Let’s say that an enterprise entered into an agreement for the supply of a large consignment of goods, but the transfer and signing of the invoice was delayed. The note also indicates an account that reflects the amount of actual costs for manufacturing the product.

Other income

This section indicates the total amount of receipts. The document also provides the amount of non-operating income and the amount of funds received from the sale of fixed assets. Based on these data, the amount of income for taxation purposes is indicated. The note explains the reasons for the difference. Other expenses are described in the same way.

Income tax calculations

The explanatory note indicates the regulatory document that guides the enterprise when calculating the obligatory payment to the budget. It is PBU 18/02. The note should indicate the specific amount of profit for tax purposes. Sources of information are tax registers and declaration information. The document describes the main operations related to the calculation of the mandatory payment. For example:

"The tax rate for 2013 is 20%. The amount of the calculated mandatory payment to the budget is 327,000 rubles. The amount of accounting profit is 470 thousand rubles. The conditional expense reflected in DB account 99.02.1 is 94 thousand rubles. The amount of deferred tax assets at the beginning of 2013 - 50 thousand rubles. During the reporting period, there was an increase in tax assets by 34 thousand rubles due to the formation of a temporary difference in the amount of 170 thousand rubles. The amount of PTA (permanent tax assets) - 10 thousand rubles. It arose due to the difference in the amount of the founding contribution of the participant owning 100% of the authorized capital. The amount of tax obligations in 2013 was 209 thousand rubles. It arose due to permanent differences - 1,045,000 rubles. profit of the enterprise, calculated in accordance with the provisions of PBU 18/02 - 327 thousand rubles, which corresponds to the information in the declaration for 2013."

Financial result of economic activity

This section also lists the specific amount received in the current year. The note lists the factors that influenced the financial result. These, in particular, may include commercial, administrative and other expenses incurred and written off relating to the sale of a large batch of finished products produced in the last quarter of the completed year and sold in the first quarter of the period that began.

Accounting Policy Data

This section indicates the regulatory documents on the basis of which it was formed and approved. The accounting policies describe:

Conclusion

The final documents, provided at the end of the period to interested users, contain dry numbers. The necessary clarifications on certain areas of accounting are provided by the explanatory note to the balance sheet. The FSS in some cases requires this document, although the regulations do not provide for the obligation of enterprises to provide it. The main users, as a rule, are the founders and the Federal Tax Service. The explanatory note can also be checked by auditors to ensure that its indicators correspond to the balance sheet figures. In practice, there are usually no difficulties in drawing up this document. Since there is no unified form, specialists use established unspoken rules for filling it out. The explanatory note must be certified by the signatures of the general director and chief accountant.